- Introduction: The Christmas Gift That Changed Everything

- Part 1: The Discovery Phase — Hunting for Clues in the Corridors of Power (2020–2022)

- Part 2: The Verdict That Split Reality (2023)

- Part 3: The Battle of the Numbers and "Judgment Day" (2024)

- Part 4: The Final Gambit and "Peace" at Any Cost (2025)

- Part 5: The Legacy of the "Case of the Century" and the World After Ripple (Today)

Introduction: The Christmas Gift That Changed Everything

Imagine the morning of December 22, 2020. The entire financial world is holding its breath in anticipation of the Christmas holidays. Wall Street is packing its bags, and crypto traders are counting the profits of a successful year. But within the offices of the U.S. Securities and Exchange Commission (SEC), the mood is different. On his last day in office, Chairman Jay Clayton signs a document that will become the start of the most high-profile legal battle in the history of digital assets.

The lawsuit against Ripple Labs was not just a legal claim. It was a planned "blitzkrieg." The SEC accused the company of selling $1.3 billion in unregistered securities. For the industry, it sounded like a death sentence for the entire idea of decentralization. If XRP is a security, then every other project is at risk.

The market reacted instantly. While lawyers were still opening case files, major exchanges panic-delisted XRP. The coin's price plummeted, erasing billions of dollars in market cap and the hopes of thousands of investors. But it was at this moment that the "victim" decided not to surrender, but to strike back — a counterattack that, five years later, would turn the hunter into the hunted.

Part 1: The Discovery Phase — Hunting for Clues in the Corridors of Power (2020–2022)

Every good detective story begins with searching for hidden motives. When Ripple Labs was backed against the wall, its lawyers chose the strategy of "the best defense is a good offense." They started digging where the regulator least wanted outsiders — into the Commission's internal correspondence.

The Prime Suspect: The Ghost of William Hinman

At the center of attention was a document that became legendary in the crypto community — the "Hinman Speech." In 2018, then-SEC Director William Hinman stated that Ethereum is not a security. Why? Because it is "sufficiently decentralized."

Ripple's defense asked a logical question: if Ethereum received a pass, why is XRP, operating on similar principles, declared illegal? The SEC tried to downplay the matter, claiming Hinman's speech was his "personal opinion," not the agency's position. But the detective mechanism was already in motion.

The Battle for the Drafts

The entire year of 2021 was spent in a grueling legal siege. Ripple demanded access to the internal drafts of this speech and SEC staff emails. The regulator resisted with the fury of the doomed, citing "deliberative process privilege" (the right of officials to keep discussions confidential).

Judge Analisa Torres, who became the key arbitrator in this battle, repeatedly rejected the SEC's protests. When the "Hinman Documents" finally came into the possession of Ripple's lawyers, something sensational was discovered. It turned out that within the Commission itself, relevant departments had warned Hinman: his "decentralization" criteria would confuse the market and create a legal vacuum.

The SEC knew about the uncertainty but preferred not to provide clear rules, opting instead for a heavy-handed approach. Ripple's argument of "Fair Notice" began to take on a steely precision: how could a company comply with a law that the regulator itself could not coherently formulate?

The Cost of War

While lawyers fought over commas in documents, Ripple continued to live under a blockade in the American market. But this was not the end. Cut off from the U.S., the company began expanding into Asia, the Middle East, and Europe. It was a paradox: a project that U.S. authorities were trying to outlaw was becoming the foundation for state payment systems around the world.

By the end of 2022, the parties approached the end of the discovery phase. Thousands of pages of text lay on the judge's table. The air smelled of a coming storm. No one yet knew that in 2023, a verdict would be delivered that would split the crypto market into "before" and "after."

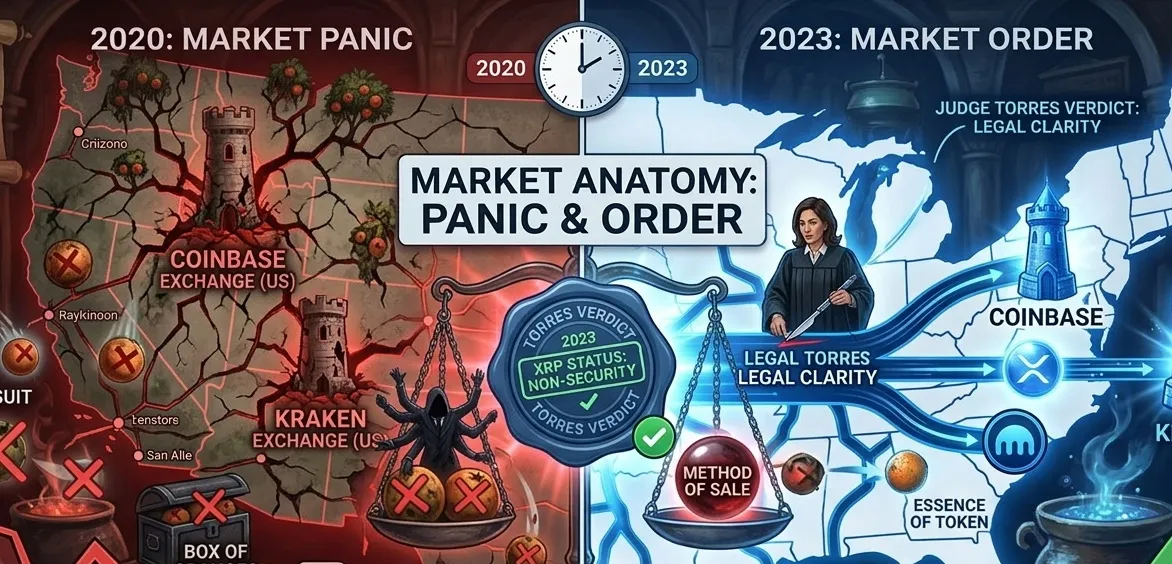

Part 2: The Verdict That Split Reality (2023)

If 2021 and 2022 were "positional warfare" in the trenches, then 2023 became the time of the main battle. The crypto community held its breath: the fate of the entire U.S. industry now depended on how one woman — Judge Analisa Torres — would interpret the Howey Test, created back in 1946 for transactions involving orange groves.

July 13, 2023: XRP's "Independence Day"

This Thursday was forever etched into history. Torres published a ruling that initially caused shock, and five minutes later, euphoria. She did what the SEC feared most: she separated the very essence of the asset from the method of its sale.

The essence of the verdict was surgically precise:

-

Programmatic Sales (to exchanges and retail): The court ruled that when an ordinary person buys XRP on an exchange, they are not entering into an "investment contract" with Ripple. The buyer doesn't even know who they are buying from — the company or their neighbor. There is no expectation of profit from the efforts of a specific party. Verdict: not a security.

-

Institutional Sales: Here, Ripple received a "yellow card." Direct sales to hedge funds under contracts were deemed sales of unregistered securities, as the funds understood what they were investing in and anticipated profits from the company's growth.

It was a legal masterpiece. XRP became the first cryptocurrency in the U.S. to receive judicial confirmation of its status: "A token itself is not a security." Exchanges, including Coinbase and Kraken, began relisting XRP the same day. The coin's price soared nearly 100% within hours.

The Collapse of the SEC's Strategy and Capitulation

The regulator tried to strike back, filing a request for an interlocutory appeal. But Judge Torres was adamant: "No." She would not allow the SEC to challenge her ruling before the entire process was complete.

But the real detective twist came in October 2023. Suddenly, without explanation, the SEC dropped all charges against Brad Garlinghouse and Chris Larsen. The regulator, which for three years had painted Ripple's executives as "egregious wrongdoers," simply laid down its weapons in the face of a potential open jury trial. It was total capitulation on the personal score.

Part 3: The Battle of the Numbers and "Judgment Day" (2024)

When the smoke cleared from the battle over the token's status, one final question remained on the battlefield: the price of atonement. The "Remedies" phase began — determining the penalty for those institutional sales that the court had deemed illegal.

The Psychological Attack for $2 Billion

In March 2024, the SEC made a shocking demand. The regulator sought a fine of $2 billion. This was an attempt not just to punish, but to bleed the company dry, to make it a cautionary tale to intimidate others.

Ripple countered with its own calculation. The company's lawyers argued that institutional buyers were "accredited investors," none of them suffered losses, and therefore the fine should be symbolic — no more than $10 million. The gap between the parties' positions was a chasm of 200 times.

August 7, 2024: The Final Judgment

The courtroom in the Southern District of New York once again became the center of the world. It was expected that Torres would either side with the regulator or prolong the process for years. But she delivered a ruling that legal circles called "a devastating defeat for the SEC masked as a fine."

-

Fine: Instead of $2 billion — $125 million. This was 16 times less than the Commission's request. For Ripple, with its billion-dollar reserves, this was a drop in the bucket.

-

No Disgorgement: Most importantly, the court denied the SEC's demand to return "ill-gotten gains." The reason? The regulator failed to prove that a single investor lost money.

-

Injunction: The court imposed a permanent injunction against future violations, but this was more of a formality, as Ripple had already restructured its sales to comply with the new rules.

The SEC tried to spin this as a victory, but the market understood correctly. Ripple's capitalization and interest in XRP began to grow based on fundamental factors. However, the detective story wouldn't end so simply. In October 2024, both parties filed appeals, preparing for the final round in the higher court.

No one knew then that the political winds in the U.S. would shift, and 2025 would bring a resolution unimaginable at the start of this journey.

Part 4: The Final Gambit and "Peace" at Any Cost (2025)

In early 2025, the atmosphere surrounding the case began to feel like the calm before the storm. The appeals court was preparing to hear the claims from both sides, and lawyers predicted another two years of grueling battle. But a factor not found in law textbooks intervened — politics.

Winds of Change in Washington

Priorities shifted within the SEC's corridors. The era of "regulation by enforcement," personified by the old leadership, began to crack under pressure from Congress and new appointments. It became obvious: continuing the war with Ripple meant continuing to embarrass itself in the higher courts.

The detective intrigue peaked in May 2025. Behind closed doors, negotiations began that culminated in a true political "explosion." Instead of waiting for the appeal decision, the parties announced a settlement agreement.

Terms of the Crypto Industry's "Brest-Litovsk Peace"

On May 8, 2025, a historic agreement was signed:

-

Final Figure: Ripple pays just $50 million — an amount that looks almost comical compared to the initial $2 billion claim.

-

Return of Funds: The remainder of the $125 million fine, previously deposited by the company, was returned to Ripple's accounts.

-

Full Pardon: Both sides withdrew all their appeals.

This was not merely "agreeing to a fine." It was an official recognition that the old system had lost. In August 2025, five years after that fateful "Christmas gift," the Ripple vs. SEC case was finally and irrevocably closed. The witch hunt was officially over.

Part 5: The Legacy of the "Case of the Century" and the World After Ripple (Today)

So, what do we have now that the dust has finally settled on the legal tomes? This case didn't just set a precedent — it rewrote the DNA of the cryptocurrency market.

1. Legal Immunity

Today, XRP is the only digital asset in the U.S. (aside from Bitcoin) with complete legal clarity. For banks and corporations, this became a decisive signal. Whereas before, financial institutions were wary of working with Ripple due to legal risks, now they are lining up. Legal purity has become its primary market asset.

2. The Golden Rain from Wall Street: The Era of XRP-ETFs

The closure of the case opened floodgates that had been locked for five years. Institutional investors, who previously watched from the sidelines, gained a legal instrument — spot XRP-ETFs. Approval of these funds became a formality immediately after the case closed. Now, capital from pension funds and insurance giants flows into the XRP ecosystem, providing liquidity that was unimaginable in 2020.

3. From Ripple Labs to a Global Empire

Freed from legal shackles, the company went on the offensive. The launch of its own stablecoin RLUSD, integration with global liquidity protocols, and preparation for an IPO — all of this became possible only because Ripple refused to compromise its principles in 2020. The acquisition of broker Hidden Road for $1.3 billion sent a clear signal: Ripple is no longer defending itself; it is building its own system capable of competing with SWIFT on a global level.

4. Significance for Other Cases

Ripple's victory became a "shield" for other crypto giants — Coinbase and Binance. Judges in their cases now look to Judge Analisa Torres's ruling: a token by itself is not a security. This deprived the SEC of its main weapon — the ability to label any digital code an investment contract.

Epilogue: A Lesson for Investors

The story of Ripple vs. SEC is not a tale of courts and fines. It is a detective story about how one company challenged the system and, despite colossal losses, emerged victorious.

For the investor, this five-year marathon carries one key lesson: fundamental value always triumphs over temporary pressure. Those who believed in the "bridge currency" technology when XRP was worth pennies under the weight of lawsuits, today see their asset becoming the standard for a new financial architecture.

Ripple has journeyed from "crypto pariah" to "institutional favorite." The war is over. The era of adoption begins, where XRP is no longer the defendant, but the legitimate king of cross-border payments. And if this detective story has taught us anything, it's that in the financial world, it's not the strongest who survive, but those who can prove they are right until the very end.