- Introduction: What is Ripple in Simple Terms?

- History and Key Figures: From Utopia to Corporation

- Technological Foundation: How Does It Work?

- XRP Tokenomics: Where Does the Value Lie?

- The Ripple Product Ecosystem: From Payments to a Global Standard

- The Great Legal Battle: Ripple vs. The SEC

- Partnerships and Real-World Application: Financial Diplomacy in Action

- Criticism and Risks: The Dark Side of the Moon

- Future Outlook and Predictions (2025-2030): The Era of Dominance

- Conclusion: The Verdict for Investors

Introduction: What is Ripple in Simple Terms?

If you ask three different people to explain what Ripple is, you will likely get three different answers. A trader will say it's a "top-10 crypto," a bank clerk will call it a "payment protocol," and until recently, a lawyer from the SEC would nervously adjust their tie at the mere mention of the word.

The main challenge for a beginner is that the term "Ripple" has become an umbrella brand, concealing three distinct, though interconnected, entities. Let's bring order to this chaos using a tech-world analogy.

1.1. The Great Trinity: The Company, The Asset, and The Ledger

To understand Ripple, imagine the company Apple.

-

Apple has iOS (the operating system that everything runs on).

-

Apple has the iPhone (the product they sell).

In the Ripple world, the architecture looks like this:

-

Ripple (The Company): This is a private commercial organization (the legal entity Ripple Labs Inc.). They have offices in San Francisco, London, and Singapore, a board of directors, and hundreds of developers. Their goal is to sell software to large banks. If Ripple Labs decided to shut down tomorrow, the company would disappear, but the technology would not.

-

XRP (The Digital Asset): This is the coin itself, the "fuel" of the system. If Ripple is the corporation, XRP is the independent digital code that lives on the network. It's a tool for transferring value. It's crucial to understand: XRP is not a share of stock in Ripple, even though the company owns a vast number of these coins.

-

XRPL (XRP Ledger): This is the "railroad track" the train runs on. It's a distributed, open-source ledger. A blockchain (technically, a distributed ledger without traditional blocks, but more on that later) where all transactions occur. It is decentralized: it's maintained by hundreds of independent nodes worldwide, not just the company's servers.

Why is this important? This decentralization became a key argument in court. Ripple Labs tried to prove that XRP could exist on its own, even if the company ceased to operate.

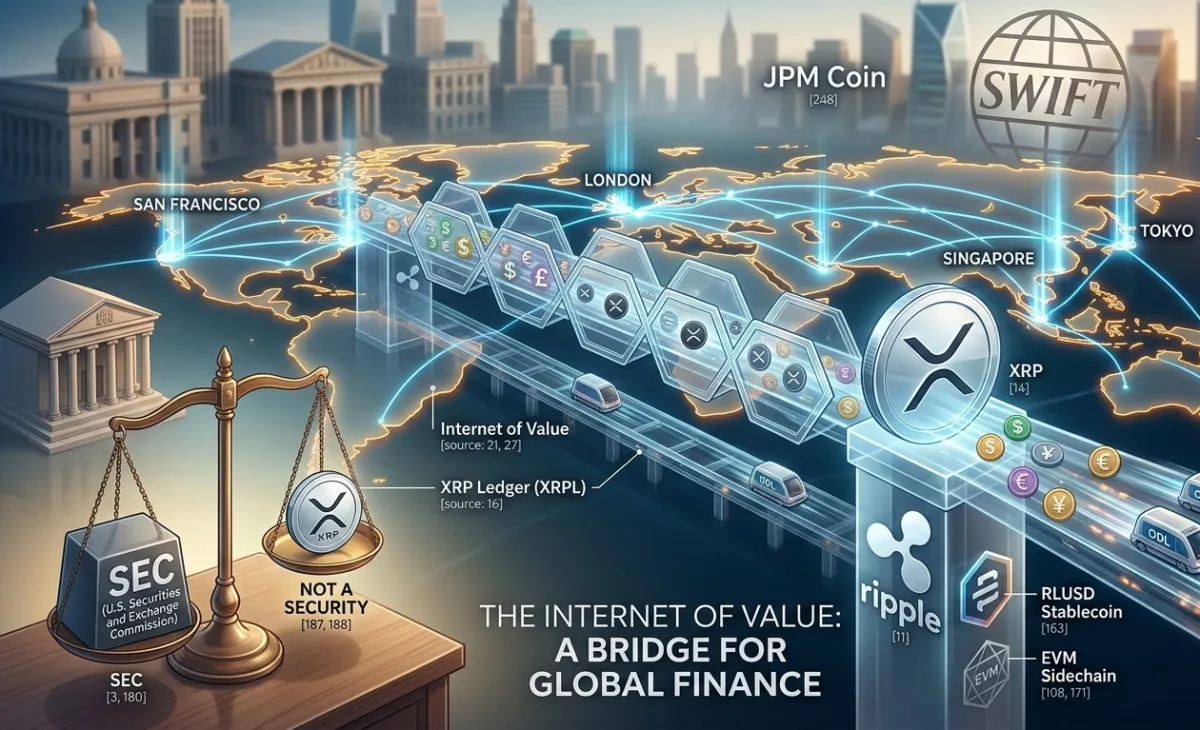

1.2. The Mission: The "Internet of Value"

Have you ever wondered why, in 2026, you can send a 4K video to a friend in Australia in a fraction of a second, but transferring money there takes 3-5 business days and costs you $30-$50 in fees?

We live in the era of the "Internet of Information," where data travels instantly. But the financial world still lives in the era of "paper mail." The SWIFT system, used by banks, is essentially a messaging system. It doesn't move money; it simply tells Bank B, "Hey, Bank A confirmed they have money for you, so adjust the numbers in your database."

Ripple's mission is to create the "Internet of Value" (IoV). The idea is simple: money should move as fast and as cheaply as a text message on Telegram. Ripple aims to eliminate the "middlemen's middlemen." Instead of routing a payment through 5 correspondent banks, the system uses XRP as a universal bridge.

Example: You send Yuan (CNY), they are instantly converted to XRP, XRP crosses the ocean in 3 seconds, and on the other side, the recipient instantly receives Dollars. No waiting for "the end of the business day."

1.3. Quick Facts: Impressive Numbers

To understand Ripple's market impact, let's look at some dry but powerful statistics.

-

Transaction Speed: 3-5 seconds. For comparison: Bitcoin takes 10 to 60 minutes, Ethereum about 15 minutes.

-

Cost: The average fee on the XRPL network is approximately $0.0002. This is so low that the network is practically free for the average user. It's a spam protection mechanism, not a revenue source.

-

Scalability: The network can handle over 1,500 transactions per second (TPS) 24/7. This puts it on par with the capacity of the Visa payment system.

-

Market Position: Since its launch in 2012, XRP has almost never left the top-10 cryptocurrencies by market capitalization. It's one of the few "veterans" (along with Bitcoin and Litecoin) that has survived dozens of boom-and-bust cycles, remaining relevant.

History and Key Figures: From Utopia to Corporation

Ripple's story isn't the typical tale of "cypherpunks" wanting to destroy banks. It's a story of people who wanted to fix banks. If Bitcoin was created as an antithesis to the financial system, Ripple was created as its upgrade.

2.1. From Idea to Realization: Ryan Fugger and the Pre-Bitcoin Era (2004)

Few know this, but the concept of Ripple predates Bitcoin. In 2004 (4 years before Satoshi Nakamoto's manifesto), a Vancouver-based programmer named Ryan Fugger developed a system called RipplePay.

His idea was philosophical and profound: "Money is simply debt and trust." RipplePay had no coins. It was a trust network. If I trust you for 100 rubles, and you trust your friend for 100 rubles, I can transfer value to your friend through you. It was a decentralized system of mutual credit.

However, RipplePay was too complex for the average user at that time. It was ahead of its era. Everything changed in 2011-2012 when new people emerged who saw in Fugger's idea the potential for creating a global payment rail.

2.2. The Birth of OpenCoin (2012) and Legendary Founders

In 2012, Jed McCaleb and Chris Larsen approached Ryan Fugger. They convinced him the system needed digital assets and a more powerful technological base. Thus, the company OpenCoin was born, later renamed Ripple Labs.

Who were the key figures at the dawn of Ripple? They are the "Avengers" of the crypto world, each with a unique (and sometimes controversial) reputation:

-

Jed McCaleb: A legendary figure. Creator of eDonkey (file-sharing network), founder of the infamous Mt. Gox exchange (which he sold before the hack), and the chief architect of Ripple. Jed is an idealist. His departure from Ripple in 2013 due to disagreements with Chris Larsen became one of the industry's biggest scandals. He later founded a direct competitor, Stellar (XLM).

-

Chris Larsen: An experienced Silicon Valley businessman. Before Ripple, he founded E-Loan, one of the first online lending services. Larsen brought a "grown-up" approach, connections in the banking world, and an understanding of how regulators work to the project. Today, he is one of the wealthiest individuals in the crypto industry.

-

Arthur Britto: The most enigmatic figure. There is almost no information about him; he doesn't give interviews and has no photos on social media. Britto is a brilliant coder who, along with McCaleb, architected the distributed ledger's logic. It's said he insisted on creating a limited supply of 100 billion coins.

-

David Schwartz (JoelKatz): The current Chief Technology Officer (CTO) and the brain of the company. David is one of the world's top cryptographers. If you see a technically complex post on the Ripple blog, chances are he wrote it. He was the one who turned McCaleb's theoretical sketches into working, secure code.

2.3. Brand Evolution and the "Banking Pivot"

Between 2013 and 2015, the company underwent a serious transformation. It became clear that simply being "another cryptocurrency" was a path to nowhere. Competing with Bitcoin for the title of "digital gold" was pointless.

Ripple Labs made a decision that for years made them pariahs in the Bitcoin maximalist community: they decided to work with banks.

-

Rebranding: OpenCoin became Ripple Labs.

-

Strategy Shift: Instead of trying to convince people to buy coffee with XRP, they approached giants like Santander, American Express, and SBI Holdings.

-

Software Products: Software packages (xCurrent, xRapid, xVia) were created. The idea was to give banks blockchain technology that integrated into their existing systems without needing to overhaul everything.

This period was a time of "building trust." While the rest of the crypto market was associated with the dark web and volatility, Ripple's leadership attended forums in Davos, wore expensive suits, and hired former officials from the U.S. Treasury and the Federal Reserve.

They were building a legal bridge between the world of fiat (traditional money) and the world of crypto. This strategy made Ripple the most "establishment-friendly" cryptocurrency, simultaneously drawing admiration from investors and ire from those who believed in complete anonymity and lack of control.

Technological Foundation: How Does It Work?

If Bitcoin is a huge, heavy, but ultra-reliable fortress, then XRP Ledger (XRPL) is a high-speed hyperloop, designed for the most efficient movement of goods (money).

3.1. XRPL: Why Isn't It a "Blockchain" in the Classic Sense?

In the crypto world, the word "blockchain" has become a generic term, but technically XRPL is a distributed ledger. What's the catch?

A classic blockchain (like Bitcoin's) is a chain of blocks, where each subsequent block is "mined" by miners. In XRPL, there is no mining. There are no blocks in the traditional sense that need to be "found" by solving mathematical problems. Instead, the network operates like a giant, shared Excel spreadsheet that updates every 3-5 seconds.

Key Difference: In Bitcoin, security is provided by energy (mining); in Ethereum, by capital (staking); and in Ripple, by trust and consensus.

3.2. The Consensus Algorithm (RPCA): Magic Without Miners

Let's break down how the Ripple Consensus Ledger (RPCA) differs from what we're used to:

-

Goodbye, Proof-of-Work (Bitcoin): Mining requires colossal amounts of electricity. In Ripple, there's no competition between graphics cards. This makes the network thousands of times cheaper and faster.

-

Goodbye, Proof-of-Stake (Ethereum): You don't need to "lock up" your coins to validate transactions and earn rewards. Ripple has no direct financial reward for supporting the network (which, incidentally, was a point of criticism for a long time).

So, how do they agree?

It all hinges on Validators and the UNL (Unique Node List).

Imagine an exclusive gentlemen's club. For a transaction to be approved, it must be confirmed by at least 80% of the club members.

-

Validators are the nodes (servers) that verify transactions. They are run by universities (MIT), exchanges, banks, and Ripple itself.

-

UNL is a list of nodes that a specific server trusts. You choose who to trust. If 80% of those trusted nodes say, "Yes, Ivan has 100 XRP and he sent them," the transaction is permanently recorded in the ledger.

3.3. Scalability: David vs. Goliath (SWIFT and Visa)

In 2026, speed is everything. While the traditional SWIFT system operates on a "send and pray it arrives in 3 days" principle, Ripple showcases remarkable performance:

| Parameter | Bitcoin | SWIFT | Visa | Ripple (XRP) |

|---|---|---|---|---|

| Transaction Speed | 10-60 min | 1-5 days | Seconds | 3-5 seconds |

| Throughput | ~7 TPS | --- | 24,000+ TPS | 1,500 – 3,400+ TPS |

| Cost | High/Medium | $20-$50 | Bank fee | $0.0002 |

*TPS = Transactions Per Second.

Thanks to the 2025 upgrade and the launch of the EVM sidechain (Ethereum Virtual Machine), XRPL can now not only transfer money quickly but also run complex smart contracts, competing with Ethereum in the DeFi (Decentralized Finance) space.

3.4. Environmental Friendliness: A Cryptocurrency with a "Green" Soul

While environmentalists in 2021-2022 were attacking Bitcoin for its "carbon footprint," Ripple positioned itself as a leader in ESG (Environmental, Social, and Governance) principles.

Because there is no mining on the network, one XRP transaction consumes about as much energy as a couple of mobile phone calls or a few hours of a light bulb. This is 61,000 times more efficient than Bitcoin. For large corporations and banks, which are now required to report on their environmental impact, this became a decisive factor in their choice.

XRP Tokenomics: Where Does the Value Lie?

The economics of XRP is perhaps the most discussed topic on Reddit and Twitter (X). It's unique, sometimes contradictory, but strictly logical from a business perspective.

4.1. Supply: Why 100 Billion from the Start?

Unlike Bitcoin, which is "mined" gradually, all 100,000,000,000 XRP were created (minted) at once in 2012.

-

No new coins will ever be created.

-

Conversely, the total supply slowly decreases (see the section on burning).

Why so many? The answer lies in the "Bridge Currency" strategy. For banks to transfer billions of dollars daily through XRP, liquidity must be abundant. If there were too few coins, the price would be too volatile for banking needs.

4.2. The Escrow System: Taming the "Printing Press"

The main fear for investors has always been: "Ripple holds a massive portion of the coins. What if they decide to sell them all and crash the market?"

To calm the market, in 2017, Ripple created the Escrow system. They locked up 55 billion XRP in a series of smart contracts.

How it works in 2026:

-

On the 1st of each month, 1 billion XRP is automatically released from escrow.

-

Ripple uses a portion of these coins (usually around 200-300 million) for sales to institutional partners and to fund development.

-

The remaining 700-800 million XRP are sent back into escrow, placed at the back of the queue (locked for another 5+ years).

This creates predictability. Investors know for sure that the company cannot dump all its coins on the market at once.

4.3. The Burning Mechanism: Deflation in Action

XRP is a deflationary asset. Every transaction on the network costs a tiny fraction of a coin (standard is 0.00001 XRP).

Important: This fee does not go to miners or to Ripple. It is simply destroyed (burned).

To date, over 12 million XRP have been destroyed. Yes, compared to a total supply of 100 billion, this seems like a drop in the ocean, but with mass network adoption (especially with the launch of the RLUSD stablecoin), the burn rate will increase. This makes XRP more valuable in the long term.

4.4. XRP as a "Bridge Currency"

This is the "holy grail" of XRP tokenomics. Imagine you want to exchange Mexican Pesos for Thai Baht. Doing it directly is difficult—banks would typically buy Dollars with Pesos first, and then Baht with Dollars. This means double fees and delays.

Ripple proposes using XRP as the intermediary:

Pesos —> XRP —> Baht

The process takes 3 seconds. Here, XRP acts as a universal "solvent" for liquidity. The more banks use this bridge, the higher the demand for the asset, and the more stable its price becomes.

The Ripple Product Ecosystem: From Payments to a Global Standard

By 2026, Ripple has completely transformed from a niche startup into a full-fledged financial infrastructure corporation. If the company's products once resembled a "construction kit" of different services, today it is a seamless ecosystem.

5.1. ODL (On-Demand Liquidity)

This is the "jewel in the crown" of Ripple. The main problem for banks with international transfers is the need to hold large sums in accounts in other countries (so-called Nostro/Vostro accounts). This is "dead capital" just sitting there to facilitate future transactions.

ODL solves this problem elegantly:

-

The bank doesn't need to pre-purchase and hold Yen, Euros, or Baht.

-

At the moment of transfer, the system uses XRP as a bridge.

-

Money is instantly converted to XRP, sent across the ocean, and converted into the target currency on the other end.

In 2025-2026, ODL became the standard for corridors between Asia, Latin America, and the Middle East. Banks freed up billions of dollars in working capital that previously just sat idle in foreign accounts.

5.2. Rebranding and Convergence: Ripple Payments

Users used to get confused by the names: xCurrent (for messaging), xRapid (for XRP), and xVia (interface). Ripple wisely consolidated everything into a single flagship product: Ripple Payments.

Today, it's an end-to-end platform that allows businesses to manage all their money flows—from fiat to crypto—in one window. Thanks to acquisitions of giants like Metaco (custody service) and Standard Custody, Ripple can now store its clients' assets itself, providing "banking-grade" security.

5.3. 2025-2026 Newcomer: The RLUSD Stablecoin (Ripple USD)

Many asked, "Why does Ripple need its own stablecoin if it has XRP?" The answer is simple: stability for corporations. Many conservative financial institutions are still wary of XRP's volatility. RLUSD is a fully USD-backed, regulated, and transparent stablecoin.

-

Why is it needed? It complements XRP. Where instant cross-border value transfer is needed, XRP works. Where price stability or on-chain storage of funds is required, RLUSD is used.

-

Result: By March 2026, RLUSD's market capitalization exceeded $1.5 billion, making it one of the fastest-growing institutional stablecoins globally.

5.4. Smart Contracts and EVM Sidechains

In 2026, XRPL is no longer just a "payments rail." With the launch of the EVM-compatible sidechain (Ethereum Virtual Machine) built on Ripple, it became possible to run any decentralized application (dApp). This opened the doors to:

-

DeFi (Decentralized Finance): Lending, borrowing, and yield farming directly within the Ripple ecosystem.

-

NFTs and RWA (Real World Assets): Tokenization of real estate, stocks, and commodities. Developers from the Ethereum world can now port their projects to Ripple in minutes, leveraging the speed and low cost of the XRP Ledger.

The Great Legal Battle: Ripple vs. The SEC

This chapter will go down in history books as "The Case That Saved the Crypto Industry in the US." The battle lasted nearly 5 years and cost Ripple over $200 million in legal fees alone.

6.1. The Essence of the Allegations (December 2020)

On Christmas Eve 2020, the SEC struck, accusing Ripple of conducting an illegal $1.3 billion securities offering by selling XRP tokens. The SEC's logic: "Investors buy XRP expecting profits from Ripple's efforts. Therefore, it's an investment contract (Howey Test)." The market reacted catastrophically: exchanges (Coinbase, Kraken, etc.) began delisting XRP en masse, and the price plummeted.

6.2. Key Turning Points and Judge Torres's Ruling (2023)

In July 2023, a historic event occurred. Judge Analisa Torres delivered a nuanced ruling that became the first major defeat for the SEC:

-

Institutional sales (directly to hedge funds via contracts) were deemed securities transactions.

-

Programmatic sales (on exchanges to the general public) were NOT deemed securities transactions.

This was a partial but monumental victory. XRP became the only digital asset in the US (besides Bitcoin) with a clear legal status.

6.3. The Finale (2025): End of the War

The legal saga officially concluded in May 2025. After a series of appeals and attempts by the SEC to prolong the process, the parties reached a final settlement:

-

Fine: Ripple paid $50 million (far less than the $2 billion initially sought by the SEC).

-

Freedom to Operate: The injunction was lifted. The company received the "green light" to operate in the US.

-

Funds Released: Approximately $75 million that Ripple had held in reserve for a potential loss were returned to the company's treasury.

6.4. Consequences: A Precedent for the World

The Ripple battle laid the foundation for the adoption of the Clarity Act (officially the Digital Asset Clarity Act) in early 2026. Now, courts and regulators use the "Ripple criteria" to distinguish genuine fraudulent schemes from beneficial technological protocols.

This success paved the way for the first-ever XRP-ETF, which was approved in late 2025, allowing institutional investors to gain exposure to the coin through traditional exchange-traded instruments.

Partnerships and Real-World Application: Financial Diplomacy in Action

In the crypto world, we often hear about "technology for technology's sake," but Ripple is a rare example of a project that, from day one, sought real contracts, not just hype. By 2026, Ripple's partner list reads like a "Who's Who" of global finance.

7.1. Banking Giants: Who's Already on Board?

Ripple doesn't try to destroy banks; it offers to make them more efficient. This strategy has allowed the company to sign agreements with over 300 financial institutions in 40+ countries.

-

SBI Remit (Japan): Perhaps Ripple's most loyal ally. Japanese giant SBI Holdings doesn't just use the technology; it has integrated XRP into cross-border payments between Japan and Southeast Asian countries (Philippines, Vietnam, Indonesia). For millions of migrant workers, this means sending money home takes seconds, not days.

-

Santander (Spain/UK): One of the first European banks to implement One Pay FX, built on Ripple's technology. This allows their customers to make international transfers with transparent exchange rates and instant confirmation.

-

Standard Chartered and HSBC: These industry titans use Ripple's solutions for liquidity management and optimizing trade finance flows in Asia and the Middle East.

Why is this important? Each such contract represents real transaction volume (utility) flowing through the XRPL network, increasing its significance and stress-testing the technology under real-world conditions.

7.2. Central Banks and CBDCs: Designing the Future of Money

If 2021 was the year of NFTs, 2024-2026 became the era of CBDCs (Central Bank Digital Currencies). Ripple recognized this trend early and created the "CBDC Private Ledger"—a specialized version of its ledger for sovereign states.

-

Palau: This tiny island nation became Ripple's "laboratory." They successfully launched a national stablecoin on XRPL, which citizens use for everyday purchases via smartphones.

-

Bhutan and Montenegro: These countries chose Ripple as a partner to develop the strategy and technical infrastructure for their digital currencies.

-

The Intermediary Role: Ripple's key feature is offering central banks a way to interoperate. If every country has its own digital currency, they will still need a "bridge" for exchange. Here, XRP again serves as a universal, neutral asset.

7.3. Competing with SWIFT: David vs. Goliath 2.0

SWIFT is the old guard. The system, created in 1973, was a monopoly for a long time. But Ripple has challenged it.

Where Ripple Wins:

-

Speed and Settlement: In SWIFT, the payment message travels fast, but the actual settlement (movement of funds) can take 3-5 days. In Ripple, the message and settlement happen simultaneously in 3 seconds.

-

Cost: Eliminating the chain of correspondent banks reduces costs by 40-70%.

-

Transparency: In Ripple, you see the payment status in real-time. With SWIFT, a payment can get "stuck" somewhere within an intermediary bank, with no one able to explain why.

Where Ripple Still Lags:

-

Network Coverage: SWIFT connects over 11,000 banks. Ripple's count is in the hundreds. The network effect is the hardest thing to overcome.

-

Trust and Conservatism: Bankers are notoriously cautious. They often prefer paying more for the old, reliable system than taking a risk on a new one associated with "crypto." However, the launch of RLUSD in 2025 significantly lowered this psychological barrier.

Criticism and Risks: The Dark Side of the Moon

No project in the crypto world faces as much harsh criticism as Ripple. And frankly, the skeptics have some valid points. For our article to be objective, we must examine these "pain points."

8.1. The Decentralization Question: How Free is XRP?

Bitcoin maximalists often label Ripple "centralized garbage." Why? It comes down to the UNL (Unique Node List) system. While technically anyone can run a node on the XRPL, in practice, most participants rely on a list of "recommended" nodes published by Ripple.

-

Critics' Argument: "If Ripple wants to change the network's rules, it can just coordinate with the key validators on its list."

-

Ripple's Response: "We control less than 5% of all nodes. The network is democratic; if the community disagrees with us, they can simply remove our nodes from their lists." Nevertheless, the company's influence over the protocol's development remains dominant, which contradicts the ideals of complete anarchy and independence preached by Satoshi Nakamoto.

8.2. Coin Concentration: The Escrow Sword of Damocles

We already mentioned the Escrow system, where billions of XRP are locked. But let's look at it from a risk perspective. Ripple still holds a significant percentage of the total coin supply.

-

"Dump" Risk: Even with the release schedule, the company sells significant amounts of XRP monthly to fund its operations. This creates constant selling pressure. Investors fear that as long as Ripple has this "endless faucet," XRP's price will appreciate more slowly than its competitors'.

-

The Jed McCaleb Problem: For many years, co-founder Jed McCaleb sold his 9 billion XRP, which weighed on the price. His wallet was finally emptied in 2022, but the "aftertaste" and fear of large holders remain.

8.3. Competition: Ripple Isn't Alone

The world doesn't stand still. While Ripple was battling the SEC, new players and technologies emerged that are hot on its heels.

-

JPM Coin from JPMorgan: The world's largest bank created its own internal settlement system on a blockchain. They don't need XRP; they have their own dollar within their system. This is a direct blow to Ripple's ambitions in the US.

-

Stablecoins (USDT, USDC): Why would a bank use volatile XRP when it can use a digital dollar? This is precisely why Ripple had to urgently launch its own RLUSD — to not lose this battle.

-

Ethereum L2s and Solana: These networks have become incredibly fast and cheap. Many DeFi projects and institutions choose them due to the massive developer ecosystem and flexible smart contracts.

Summary of Risks: Ripple is in a unique position — it's too big to disappear, but its path to absolute dominance is blocked both by regulators and powerful competitors from the world of traditional finance.

Future Outlook and Predictions (2025-2030): The Era of Dominance

If the previous decade was a time of struggle for survival and legal recognition for Ripple, the period up to 2030 promises to be an era of expansion. We are at a unique point in history where technology, politics, and big money have finally aligned.

9.1. Institutional Adoption: On the Threshold of an XRP-ETF

After Bitcoin-ETFs and then Ethereum-ETFs took the market by storm in 2024, the question of a similar instrument for XRP became a matter of "when," not "if."

By early 2026, the situation had changed dramatically:

-

XRP-ETF Launch: Now, major pension funds and insurance companies can buy XRP with a single click on the stock market, without dealing with wallets and private keys. This created a "constant vacuum cleaner" for liquidity, gradually sucking coins off exchanges.

-

Wall Street in Action: Firms like BlackRock and Fidelity no longer whisper about Ripple in the hallways. They include XRP in their diversified crypto baskets as an asset with the highest "regulatory clarity" in the US.

9.2. The Political Factor: Winds of Change in Washington

2025 was a turning point for the US crypto industry. The change in administration and the departure of Gary Gensler as SEC Chair marked the end of the "regulation-by-enforcement" era.

-

Strategic Crypto Reserve: In 2026, the idea of creating a national digital asset reserve is being seriously discussed at the Congressional level. If Bitcoin plays the role of "digital gold," XRP is being considered a potential "digital settlement standard."

-

Ripple's Lobbying: The company spent years building relationships in Washington. Today, Ripple is not seen as "rebels" but as respected consultants, helping to draft the rules for stablecoins and cross-border payments.

9.3. Technological Roadmap: More Than Just Payments

XRPL in 2026 is a boiling cauldron of innovation. David Schwartz's team hasn't been idle:

-

Native Lending Protocol: A built-in lending protocol has been integrated into the ledger. You can now lend your XRP for interest directly on the blockchain, without intermediaries or centralized platforms.

-

NFT 2.0: The NFT sector on Ripple has moved beyond "monkey pictures." It is now a market for RWA (Real World Assets). Tokenized bonds, real estate rights, and even invoices from major corporations now move across the XRPL with the same ease as the coins themselves.

-

Scaling: Thanks to sidechain technology, the network's throughput has theoretically become unlimited, allowing it to serve not only banks but also micro-payments for the Internet of Things (IoT).

Conclusion: The Verdict for Investors

We've come a long way, from Ryan Fugger's idea in 2004 to the modern Ripple Payments ecosystem. It's time to summarize.

10.1. Final Summary: Who is XRP For?

Ripple (XRP) is not an asset for everyone. If you're looking for a "shitcoin" that will pump 1000x overnight based on an Elon Musk tweet, you've probably come to the wrong place.

XRP is suitable for you if:

-

You are a "strategic holder": You understand that infrastructure projects grow over years, but they have real fundamentals.

-

You believe in symbiosis, not revolution: You're not waiting for the banking system to collapse; you want to profit from its upgrade.

-

You value legal clarity: After the victory over the SEC, XRP is one of the safest assets from a legal perspective.

You should be cautious if:

-

You cannot tolerate any form of centralization.

-

You are afraid of Ripple's control over part of the coin supply.

-

You seek complete anonymity (XRP is a transparent network for legitimate business).

10.2. Ripple's Place in the Future: "Bridge" or "Foundation"?

The answer to this question has already been given by history. Ripple did not become the bank killer that radicals predicted. It became their best version.

In the financial system of 2030, Ripple is both a bridge and a foundation.

-

It is a bridge because without a neutral asset like XRP, the world risks drowning in "digital islands" (fragmented CBDCs from different countries).

-

It is a foundation because the XRPL technology has proven robust enough for sovereign currencies and international settlement hubs to be built upon it.

Final Word: Ripple has been through fire, water, and the wringer (courtesy of the SEC's lawyers). It survived where others would have broken. And today, looking at the XRP price chart, we see not just numbers, but the result of fourteen years of work towards creating an "Internet of Value." The future of finance is already here, and it speaks the language of the Ripple protocol.