1. Introduction: Why Your Business Is Losing Money on Payments in 2026

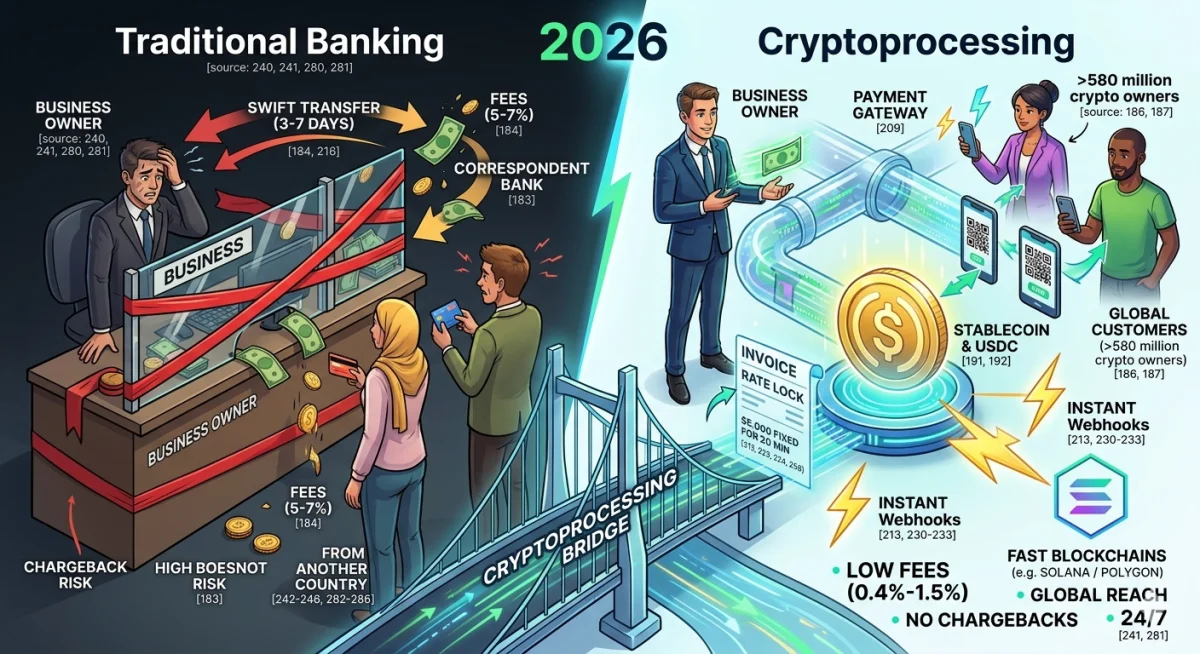

Picture a typical situation: your client from another country wants to book a hotel in a resort region or pay for a subscription to your service. They are ready to give you their money right now. But an “invisible wall” of traditional banking stands in the way. A SWIFT transfer can take a week, a correspondent bank may “freeze” the payment for review, and currency conversion plus cross-border fees can eat up to 5–7% of the amount. The result: the client is unhappy, and you lose profit.

The financial world has changed in 2026. Today, more than 580 million people worldwide own cryptocurrency. It is no longer a toy for geeks but a real payment instrument. Major players like Microsoft, Tesla, and Shopify have long integrated crypto payments because they realized: this is the fastest way to receive money from anywhere in the world without slow bank intermediaries.

Why right now? The main trend of 2026 is the explosive growth of stablecoins, especially USDC. While businesses used to fear Bitcoin because its price could drop 10% in an hour, stablecoins have solved that problem. 1 USDC always equals 1 US dollar. It is digital currency with the reliability of fiat but the speed of the internet.

Crypto processing is the technological bridge that allows your business to accept such payments legally, quickly, and securely. In this article, we will break down how to stop depending on bank whims, bypass sanctions barriers, and save on fees using tomorrow’s technologies today.

2. What Is Crypto Processing? Understanding the System’s Engine

Many business owners confuse a regular crypto wallet with processing. This is like comparing a personal wallet in your pocket with a full-fledged cash register and terminal in a supermarket.

Crypto wallet — is just a place to store coins. If you give a client your wallet address, you will have to manually check whether they sent the correct amount, used the right network, and when the payment arrived. For a business with dozens of transactions per day, this becomes an operational nightmare.

Crypto processing (or crypto acquiring) — is an automated system that handles all the routine tasks. It generates invoices, tracks blockchain confirmations, converts currencies, and provides you with detailed reports for accounting.

What does it look like for a business?

There are two main scenarios that solve different tasks:

-

“Crypto → Fiat” model: The client pays with cryptocurrency, and you receive familiar euros, dollars, or zloty in your bank account. This is ideal for companies that need to pay taxes and salaries in fiat without diving into blockchain details.

-

“Crypto → Crypto” model: You accept payment in crypto and keep it in digital assets (for example, in USDC). This is the best path for international B2B settlements: you receive payment from a US client and within 15 minutes use those same funds to pay a freelancer in Asia or purchase goods.

What does the system consist of?

For everything to work like clockwork, several components interact inside the processor:

-

Payment Gateway: What the client sees — a stylish payment window with a QR code and amount.

-

Payment Processor (Backend): The “brains” of the system. It verifies the transaction on the blockchain, locks the exchange rate, and instantly notifies your website that the goods can be shipped.

Mini-glossary for the boss: Invoice — an electronic bill for payment. Rate Lock — fixing the exchange rate. The client sees the crypto amount, and it will not change for 15–20 minutes while they make the transfer. Webhook — an instant signal from the system to your website: “Money received, grant access to the service!”.

3. How Crypto Processing Works: Step-by-Step Mechanics

Let’s walk through the payment journey with a concrete example. Imagine you sell luxury tours, and a client from Germany wants to book a villa in Bali for 5,000 USDC. In the past, they would go to a bank, fill out currency control paperwork, and you would refresh your online banking page for three days waiting for the transfer.

With crypto processing, everything happens over a cup of coffee. Here is what this path looks like “under the hood”:

-

Step 1. Selecting the method at checkout — At the payment stage, the client sees a “Pay with crypto” button. When clicked, the system doesn’t just give a wallet address — it starts a complex interaction with the blockchain.

-

Step 2. Generating a “smart” invoice — The system instantly creates a unique invoice. It contains the exact wallet address, a QR code for quick scanning, and the amount. If your store price is in dollars, the processor automatically converts it to USDC or BTC at the current rate.

-

Step 3. Rate Lock — This is a critical moment for the business. The system locks the price, typically for 15–30 minutes. During this time, the client can open their wallet app and confirm the transaction, knowing the amount will not change.

-

Step 4. Sending and validation on the blockchain — The client scans the QR code and sends the money. At this moment, the transaction enters the blockchain. For stablecoins like USDC on fast networks (Solana, Polygon), a single network confirmation is enough for the payment to be considered successful. This takes from a few seconds to a couple of minutes.

-

Step 5. The magic of webhooks — As soon as the blockchain confirms the transaction, the processor sends a webhook to your website — an instant notification. Your website’s system “hears” this signal and automatically changes the order status to “Paid”. The client immediately receives a voucher by email, and you receive a sale notification. No manual control.

-

Step 6. Settlement and conversion — Depending on your settings, the funds either remain in cryptocurrency in your secure wallet or are automatically converted to fiat (euros or dollars) for withdrawal to your company’s bank account.

How to integrate it? Businesses don’t need to hire a team of blockchain developers. Today there are three simple paths:

-

Ready-made plugins: For popular engines like WooCommerce, Shopify, or Tilda. Installation takes 15 minutes.

-

Payment links: Perfect for social networks or messengers. Create a link in your dashboard, send it to a client via WhatsApp — get paid.

-

API: For large projects with unique design and logic.

4. Business Value: Crypto Processing vs. Traditional Bank Acquiring

If you have ever faced chargebacks or account freezes because your business seemed “risky” to a bank, you will appreciate the difference. The banking system is a clunky overlay of rules from 20 years ago. Crypto processing is a financial highway.

The table below clearly shows why crypto payments are more profitable than the classic approach in 2026:

Comparative Analysis of Payment Systems

| Parameter | Crypto Processing (based on USDC) | Traditional Bank Acquiring |

|---|---|---|

| Fees | 0.4% – 1.5% (you save up to 80% on transactions) | 2% – 5% (depends on region and card type) |

| Chargebacks | Impossible. The blockchain transaction is final. | Up to 1–2% of turnover can be disputed by the client. |

| Time to receive funds | 15–60 minutes. Money is immediately at your disposal. | 2–7 business days (T+3 or T+7 system). |

| Geographic reach | The whole world. No borders or banks’ sanctions filters. | Limited to the country of registration and Visa/Mastercard networks. |

| Operating hours | 24/7/365. The blockchain never takes weekends or holidays off. | Only during banking hours. |

| High-risk industries | ✅ Yes. Ideal for iGaming, IT services, and crypto projects. | ❌ Denied. Banks often block such payments. |

| Volatility risk | None. With USDC, you work with a digital dollar. | Not applicable. |

What is the main pain point of classic acquiring? The main problem with banks is the risk of chargebacks. In traditional acquiring, a client can dispute a payment a month after the purchase, claiming “the goods never arrived”. The bank often takes the client’s side, freezes your money, and issues a fine. With crypto, this is technically impossible. If a transaction is confirmed on the blockchain — the money is yours. This gives businesses tremendous peace of mind.

Moreover, for companies in the High-risk segment (e.g., international gambling or complex IT solutions), crypto processing is often the only way to legally accept payments, as banks routinely refuse to serve such sectors.

Conclusion: Crypto processing is not just a “cool feature”. It is a way to reduce costs by 3–5 times and forever forget about payment delays and the whims of large banks’ compliance departments.

5. Advantages and Disadvantages: An Honest Look at Numbers and Risks

In business, there are no “magic pills”, and crypto processing is no exception. To help you make an informed decision, let’s break down the pros and cons without marketing gloss.

✅ Advantages that change the game

-

Savings on fees: On average, payment acceptance costs are reduced by 3–5 times compared to bank acquiring. If a bank takes up to 5% of turnover, a crypto gateway will cost you 0.4–1.5%.

-

Protection against “consumer terrorism”: Crypto has no chargebacks whatsoever. A client cannot press a button in their banking app and reverse a payment after they have already used your service.

-

Instant B2B payments: Forget about SWIFT and multi-day waits. You can pay a global freelancer or purchase goods, and the funds will arrive in minutes.

-

Stability of the digital dollar: Using USDC completely removes the main fear of businesses — volatility. You receive an asset tightly pegged to the US dollar.

-

Speed of implementation: Integrating a payment button on a website often takes a few hours, not weeks as with a bank agreement.

❌ Disadvantages and risks (important to know)

-

Regulatory barriers: Not all countries have transparent legislation yet. In some jurisdictions, working with crypto is still in a “gray” zone or completely prohibited.

-

Gas fees: At peak times, network congestion (especially Ethereum) can make a transaction expensive. However, modern solutions based on Solana or Polygon reduce these costs to pennies.

-

Cost of error: If a client sends money on the wrong network (e.g., confuses token standards), it is nearly impossible to recover. Modern gateways try to block such attempts at the address entry stage, but human error remains.

-

Verification requirement (KYB): For serious business, there is no anonymity. To withdraw funds to fiat and operate legally, you will need to go through a Know Your Business procedure, providing company documents.

6. Who Needs Crypto Processing? Industries and Real Cases

Crypto processing is a lifeline for those who operate globally or face bias from traditional banks.

Target niches for implementation:

-

E-commerce (International sales): If your store sells products worldwide, crypto is the easiest way to accept payment from a client whose card is not supported by your local payment system.

-

iGaming and Betting: Industries that banks often label as “High-risk” and refuse service without explanation. For them, crypto processing is the gold standard for survival and growth.

-

SaaS and IT services: Global software subscriptions are easiest to pay for in digital dollars, avoiding double currency conversion.

-

Travel & Tourism: Imagine a traveler who wants to pay for a hotel directly, bypassing aggregators with their huge markups. Crypto payment here is the fastest and cheapest path.

-

Luxury Goods and Real Estate: When dealing with large tickets, bank transfer fees can amount to thousands of dollars. With crypto, a million-dollar transfer costs the same as a hundred-dollar one.

-

When is crypto processing NOT needed? If you have a purely local offline business (e.g., a coffee shop in a residential area) where all customers pay with local cards. If you are registered in a country where cryptocurrencies are officially banned by law (e.g., China).

Real-life case study: A large e-commerce company shifted a portion of its cross-border settlements to USDC processing. The result: the average fee on incoming payments dropped from 5% to 1%, and the problem of unjustified chargebacks disappeared entirely. This allowed the company to save tens of thousands of dollars monthly on operational expenses alone.

7. Entry Gates: How to Apply and What to Prepare

If you have decided that crypto processing is right for your business, it is important to understand: this is not just installing a “donation plugin” — it is a full-fledged financial partnership. To operate legally and have the ability to withdraw funds to fiat (to a bank account), you need to go through the “front door” of compliance.

Basic business requirements

In 2026, providers value their licenses, so they only work with transparent projects. Here is a basic checklist of what you need:

-

Legal entity: You must be registered as an LLC, sole proprietor, corporation, or Ltd. Working with “individuals” in serious processing is practically excluded.

-

Real product: You must have a working website or service with a clear monetization model.

-

Transparency: You must be ready to disclose the ownership structure and ultimate beneficial owners (UBO).

-

Clean reputation: The business and its owners must not be under international sanctions.

Document package (KYB Standard)

For “Know Your Business” (KYB) verification, you will typically need scans of the following documents:

-

Certificate of company registration and current charter.

-

Extract from the commercial register (fresh, no older than 3–6 months).

-

Passports of beneficiaries and directors, sometimes — proof of residential address.

-

Brief description of the business model: what you sell, which countries your clients come from, and what crypto turnover you expect (forecast).

What does the onboarding process look like?

Typically, it takes from a couple of days to two weeks:

-

Application: Fill out a form on the provider’s website (website, industry, turnover).

-

Pre-check: The system checks your website for compliance within 24–48 hours.

-

KYB verification: You upload documents, and lawyers verify them.

-

Agreement and integration: After approval, you sign the contract and receive API keys or plugins.

-

Launch: A test payment — and you are live.

Important to remember: If you are promised payment acceptance with fiat withdrawal without any documents at all — it is likely a “gray” service that could freeze your money at any moment without explanation.

8. Law and Order: Legal Aspects and Taxes

Crypto processing in 2026 is not a way to avoid taxes, but a way to optimize payment logistics. To sleep soundly, you need to understand the rules of the game.

Licenses and security — your main shield. A licensed processor is required to conduct KYC checks (of your clients) and use AML tools. This means the system itself checks incoming transactions: if someone tries to pay for your product with “dirty” bitcoins from the darknet, the system will simply reject that payment, protecting your reputation with banks and regulators.

How to pay taxes? Although laws vary from country to country (from Poland to the UAE), the general logic is as follows:

-

Income recognition: Received USDC or other assets are recognized as income at the exchange rate on the transaction date.

-

Reporting: Modern processors provide detailed statements and invoices that your accountant can attach to your tax return just like regular bank statements.

-

Recommendation: Always consult with a local accountant who understands the specifics of “digital assets” in your country. In most jurisdictions, stablecoins are treated as goods or digital property.

Using crypto processing makes your business modern and “white”. You are not just accepting crypto — you are doing it through a legal gateway that handles all the complexities of blockchain monitoring and fund cleanliness checks.

9. Technical Security: How Crypto Processing Protects Your Money

If a traditional bank is a fortress with thick walls and slow guards, then modern crypto processing is a smart laser security system. In 2026, security has gone far beyond a simple “login password”.

Artificial Intelligence guarding transactions — the main trend of recent years — AI monitoring. The system doesn’t just wait for blockchain confirmation; it analyzes behavior. For example, if a client from London suddenly tries to pay for a product with a wallet that was “seen” in suspicious activity in Asia just 5 minutes ago, the neural network will instantly flag that payment as risky. This is called adaptive monitoring: the system learns on the fly and catches fraudsters more effectively than any bank clerk.

Whitelists and API protection

-

IP whitelisting: You configure the system so that it only accepts commands from your server. Even if a hacker obtains your access keys, they cannot use them from another computer.

-

Two-factor authentication (2FA): Any important action — withdrawing funds or changing settings — requires confirmation via phone or biometrics.

-

Multi-signature: This is when withdrawing a large amount requires confirmation not from one person but, for example, from two — the owner and the CFO. This completely eliminates the risk of “single employee error”.

Where are the keys stored? (Custodial vs. Non-custodial approach) — an important technical choice:

-

Custodial services: The provider stores the private keys. This is convenient: if you lose your password, support can help you recover it.

-

Non-custodial services: The keys are only with you. This offers maximum security (no one, not even the provider, can touch your money), but also maximum responsibility — losing the key means losing the money forever.

10. The Future of Crypto Processing: What to Expect in 2026–2030

We are at a point where crypto is finally ceasing to be an “alternative” and is becoming part of the global financial standard. Here are three major changes that will happen in the coming years:

-

1. USDC as the new corporate standard — By 2028, the majority of international B2B transactions among small and medium businesses will shift to USDC. This will happen because corporations need predictability. Why pay huge fees to banks for a dollar transfer when you can send a digital dollar for 10 cents and receive it instantly? Stablecoins will become as common as a bank account.

-

2. Lightning Network and instant micropayments — The Lightning Network technology already allows sending Bitcoin almost for free and at messenger-like speed. Imagine paying for coffee or a digital newspaper with crypto in less than a second. By 2030, this technology will be built into every payment terminal, and the difference between “card” and “crypto wallet” for the average buyer will finally disappear.

-

3. Integration with traditional banks — We will see the “great unification”. Banks will stop fighting crypto processing and start embedding it into their apps. In 2027, your personal account in a regular bank will likely have a “Crypto Assets” tab, where you can accept payments from clients and instantly transfer them to employee payroll cards.

Forecast: The era of Web3 and “invisible” payments — By 2030, payments will become “invisible”. Inside metaverses, online games, or professional platforms, payments will happen automatically via smart contracts. Crypto processing will become the invisible layer that ensures trust between people from different countries, even if they have never met in person.

Section summary: If today crypto processing is your competitive advantage, by 2030 it will become a mandatory condition for survival in the market.

11. Conclusion: Crypto Processing Is Not the “Future” — It’s Your Profit Today

The financial world has finally split into two camps. In the first — those who continue to pay 5% fees, wait weeks for transfers, and wonder whether the bank will approve another cross-border transaction. In the second — companies that use USDC-based crypto processing and receive money instantly, from anywhere in the world, with minimal costs.

In 2026, accepting crypto has ceased to be a sign of “gray” schemes. On the contrary, it is a sign of a technologically advanced, transparent, and efficient business. If your project is focused on the international market, operates in IT, tourism, or High-risk — implementing crypto acquiring is no longer a luxury but a basic condition for maintaining margins.

Main takeaway: Don’t wait for your competitors to be the first to offer clients convenient digital dollar payments. Start small — add a payment link or one stablecoin payment method, and you will see how your life becomes easier and how client loyalty from abroad grows.

Your action plan for the next 24 hours:

-

Estimate the share of your foreign clients.

-

Check your website against the minimum requirements (Section 7).

-

Submit a consultation request to Paycot to get individual fee terms.

12. Bonus Block: Is Your Business Ready? (Checklist)

To leave you with no doubts, we have prepared a practical toolkit for a final check.

Checklist: Readiness for launching crypto processing

Check yourself against these 5 points. If you have at least 4 “Yes” answers — it is time to connect.

-

☑️ Legal entity exists: You operate as a registered company (regardless of jurisdiction).

-

☑️ Clear product: Your website is active, with a description of goods/services and a clear offer.

-

☑️ Turnover from $10,000: At such volumes, fee savings become truly noticeable for the budget.

-

☑️ International focus: Your clients or partners are in different countries.

-

☑️ Documents at hand: You are ready to spend 30 minutes uploading scans for KYB verification.